If you’re struggling to keep up with your personal loan EMIs, you’ve probably come across two very different-sounding solutions: restructure the loan, or settle it. Both promise relief — but they work in completely different ways, cost you differently, and leave a very different mark on your credit history.

Choosing between personal loan settlement vs EMI restructuring without understanding the difference is one of the most common — and costly — mistakes borrowers make when they’re already under financial stress. This guide breaks down exactly how each option works, so you can pick the one that actually fits your situation.

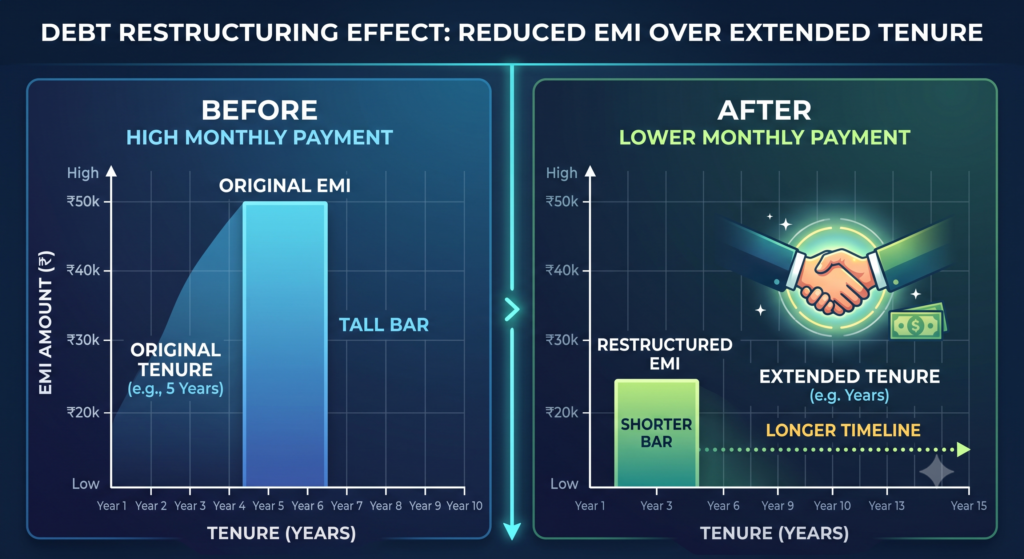

What Is EMI Restructuring?

EMI restructuring means your lender changes the terms of your existing loan — usually by extending the tenure, reducing the interest rate temporarily, or offering a moratorium (payment pause) — so your monthly EMI becomes smaller and more manageable.

Importantly, you still owe the full amount. Restructuring doesn’t reduce your debt; it just spreads it out or delays it so it’s easier to pay each month. The RBI’s resolution framework for stressed loans allows banks to offer this to genuinely distressed borrowers, though banks apply their own eligibility criteria within it.

What Is Personal Loan Settlement?

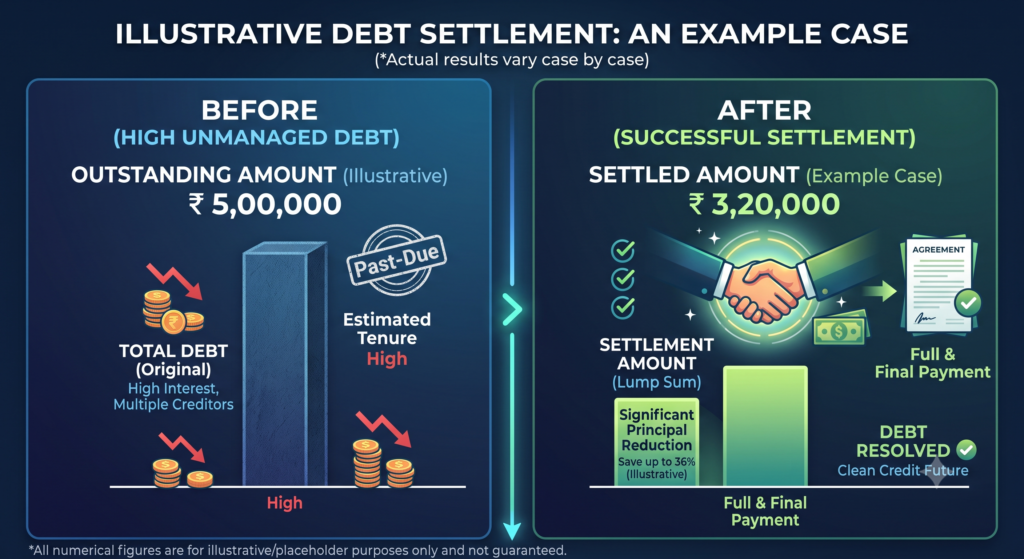

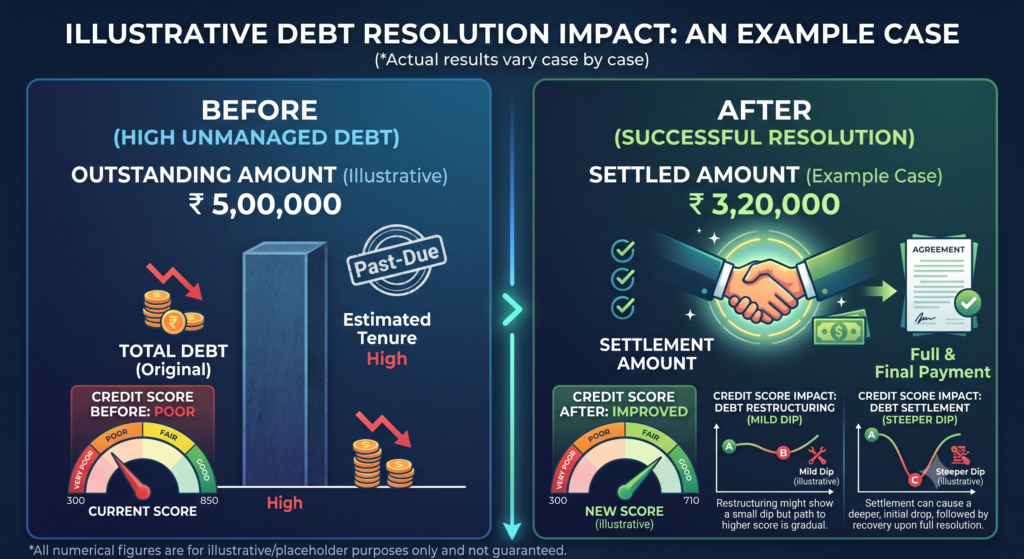

Loan settlement is different: it involves negotiating with your lender to accept a reduced lump-sum amount as full and final payment, instead of the total outstanding balance. Once the lender agrees and you pay the settled amount, your loan is marked “settled” and closed.

Unlike restructuring, settlement genuinely reduces the total amount you owe — but it comes with a more serious credit report impact, which we’ll cover below. If this is your first time exploring the option, our complete honest guide to loan settlement in India is a good starting point before you go further.

Personal Loan Settlement vs EMI Restructuring: 7 Key Differences

| Factor | EMI Restructuring | Loan Settlement |

|---|---|---|

| What changes | Loan terms (tenure, rate, moratorium) | Total amount owed is reduced |

| Do you pay less overall? | No — you pay the full principal, often with more interest over a longer term | Yes — you pay less than the outstanding balance |

| CIBIL impact | Mild — loan shows as “restructured,” recoverable over time | Severe — loan shows as “settled,” stays on record for years |

| Best suited for | Temporary income disruption (job loss, medical event) | Long-term inability to repay in full |

| Future loan eligibility | Easier to get new credit later | Harder — lenders view “settled” status cautiously |

| Process time | Faster, usually handled directly with your bank | Takes longer — involves negotiation, often through a professional |

| Who it works best for | Borrowers confident they can resume full payments eventually | Borrowers in a genuine debt trap with no realistic repayment path |

How Each Option Affects Your CIBIL Score

This is where most borrowers get the decision wrong — they focus only on which option is “cheaper” this month, without weighing the credit impact.

- Restructuring shows on your credit report but is generally viewed less harshly, since it signals you’re actively managing the situation with your bank rather than defaulting.

- Settlement is marked distinctly as “settled” (not “closed”) on your CIBIL report, and this status can make it noticeably harder to get approved for credit cards or loans for a few years afterward.

If preserving your credit score matters more to you right now than reducing the total debt, restructuring is usually the safer first step. If the debt itself has become unmanageable regardless of restructuring, settlement may be the more realistic path forward — even with the credit trade-off.

When Should You Choose EMI Restructuring?

Restructuring tends to make more sense when:

- Your income drop is temporary — a job change, medical event, or short-term business disruption

- You’re confident you can resume full EMI payments within a reasonable period

- You want to avoid a “settled” mark on your credit report

- You’re only slightly behind, not deeply overdue across multiple loans

When Should You Choose Loan Settlement?

Settlement tends to make more sense when:

- You’re behind on multiple unsecured loans or credit cards, not just one

- Recovery agents are already calling regularly — if this is happening to you, our guide on how to talk to recovery agents legally covers exactly what to say in the meantime

- Restructuring has already been tried and the EMI is still unaffordable

- You need a genuine reduction in the total amount owed, not just smaller monthly payments

- The pressure from recovery calls or visits has become a daily source of stress — our Recovery Call Handling and Stop Recovery Visits & Legal Support services exist specifically for this stage

Can You Try Restructuring First, Then Settlement Later?

Yes — and this is actually a common and reasonable path. Many borrowers approach their bank for restructuring first. If the restructured EMI still proves unaffordable after a few months, settlement becomes the next realistic option. There’s no rule against moving from one to the other, though it’s worth approaching a lender or a settlement professional with the full picture from the start, rather than after multiple missed payments pile up.

If you’re specifically dealing with credit card debt rather than a personal loan, the comparison works slightly differently — see our complete guide to credit card settlement in India for that scenario. And if you’re unsure what happens if you simply stop paying altogether without choosing either option, read what happens if you stop paying EMI in India.

Frequently Asked Questions

Is EMI restructuring the same as a loan moratorium? Not exactly — a moratorium is a temporary payment pause, while restructuring is a broader change to your loan terms that can include a moratorium as one component, along with a longer tenure or revised interest rate.

Does loan settlement affect my ability to get a home loan later? It can. Since settlement status remains visible on your credit report for a period of time, some lenders may ask about it or apply stricter scrutiny during future loan approvals. It doesn’t make future credit impossible, but it does add friction.

Which option costs less overall — settlement or restructuring? Settlement typically reduces the total amount you pay, since you’re settling for less than the outstanding balance. Restructuring usually means paying the full amount, sometimes with additional interest due to the extended tenure.

Do I need a professional to negotiate a settlement, or can I do it myself? You can approach your lender directly, but banks are generally not incentivised to offer their best settlement terms to individual borrowers negotiating alone. A professional negotiator who handles this regularly, like Loan Maaf, typically has a clearer sense of what a lender will realistically accept.

Not Sure Which One Fits Your Situation?

Every case is different — your loan type, how far behind you are, and your income outlook all affect whether restructuring or settlement is the right call. Loan Maaf has helped borrowers across India navigate exactly this decision, and can walk you through both options based on your specific numbers.

Browse more guides on our blog, see our full range of services, or once your case is resolved, our Debt Closure & No-Dues Assistance service ensures you get formal closure documentation.